UK mortgage rates are around 3.63% to 4.44% for fixed deals in March 2026, but the gap between what different lenders offer is unusually wide. This means shopping around could save you hundreds of pounds a year. This guide explains why, what rates look like right now, and how a mortgage broker can help you find the best deal for your situation.

Mar 9, 2026

Whether you are buying your first home or remortgaging, getting the right mortgage rate is one of the most important financial decisions you will make. Even a small difference in your interest rate, say 0.25%, can add up to thousands of pounds over the life of your loan.

Right now, in March 2026, that difference between lenders is bigger than usual. Some lenders are starting to raise their rates following global events, while others are holding firm. That creates a real opportunity for anyone who takes the time to compare their options properly, and a real risk for anyone who does not.

This guide will walk you through everything you need to know: what UK mortgage rates look like today, what experts predict for the rest of 2026, and how to make sure you are getting the best rate available to you.

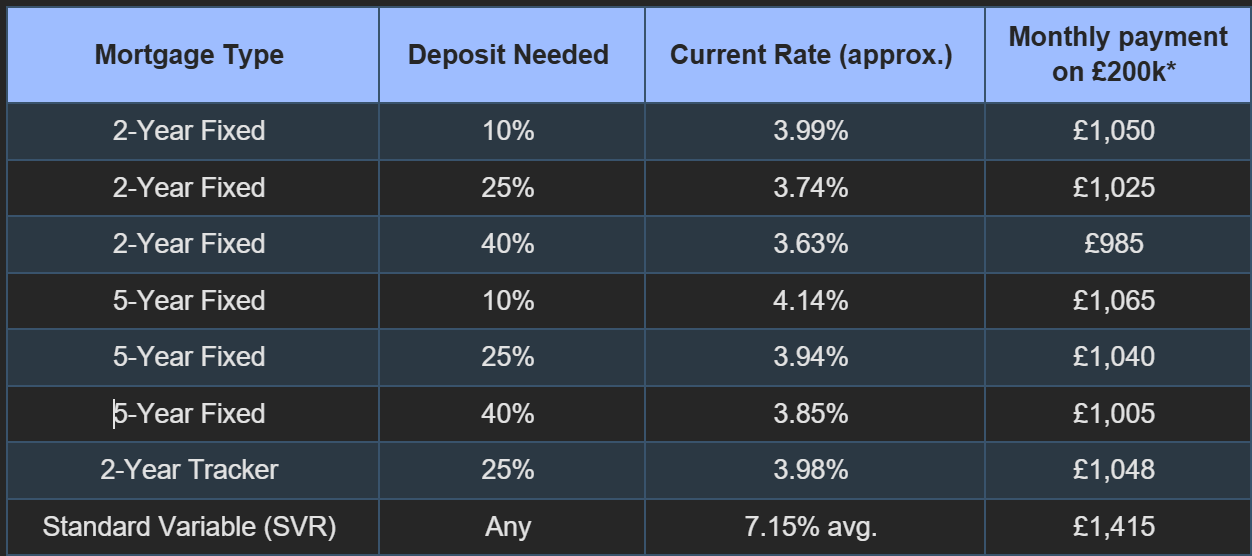

Mortgage rates have been falling gradually since their peak in 2023, and as of March 2026, the market looks more stable than it has for several years. Here are the current best rates available in the UK, based on data from L&C Mortgages (updated 9 March 2026):

The most important row in that table is the last one. The average Standard Variable Rate (SVR) in March 2026 is 7.15%. That is the rate you automatically move on to when your fixed or tracker deal ends, and most people have no idea how much extra they end up paying by doing nothing.

Important: If your current mortgage deal is ending in the next 3 to 6 months, you need to start looking now. Rolling onto your lender's SVR could cost you hundreds of pounds more every single month.

You may have seen headlines in recent days about lenders raising their fixed rates. Nationwide, HSBC and Virgin Money are among the lenders that have increased rates. So what is going on?

The short answer is global events. The conflict in the Middle East has pushed up energy prices, which raises the risk of inflation. When inflation is expected to rise, it becomes more expensive for lenders to fund mortgages, and they pass that cost on to customers.

David Hollingworth, mortgage expert at L&C Mortgages, explained it this way: the Middle East conflict has led to expectations of higher inflation, which slows down interest rate cuts and pushes up the cost for lenders when pricing their fixed deals.

The key point here is that once one major lender raises rates, others tend to follow quickly. That is why experts are saying that if you are planning to take out or switch a mortgage soon, acting sooner rather than later is sensible.

Rates could reverse the progress made in recent weeks if lenders continue to follow each other upwards. Locking in a rate now, even if you complete in several months, gives you protection against further rises.

Despite the short-term pressure, the overall outlook for 2026 remains more positive than the past two years. Here is what the main forecasters are saying:

The Bank of England has been gradually cutting its base rate after the historic hikes of 2022 and 2023. Further cuts are expected in 2026, though at a cautious pace. The pace of cuts will depend heavily on inflation data and global economic conditions.

For the UK specifically, the picture looks broadly similar. Average 2-year fixed rates were around 4.30% in early March 2026, which is 0.54% lower than the same point last year. The average 5-year fixed rate sits at around 4.44%.

Rates are expected to stay broadly stable or ease slightly. Sharp cuts are unlikely unless inflation falls faster than expected. That means the rate you can get today is not dramatically different from what you might get in 6 months, so there is little reason to wait if you need a mortgage.

Here is something many people do not realise: two people with identical financial situations can walk into different lenders and be offered very different interest rates.

That is because every lender sets their rates based on their own costs, their appetite for new business, how much risk they want to take on, and how much competition they are facing. Right now, the spread between the best and worst deals is unusually wide.

Think of it this way: if you walked into a car dealership and accepted the first price without negotiating or checking elsewhere, you would probably overpay. Mortgages work the same way. The first rate you are offered is rarely the best one available to you.

Lenders assess your application differently too. Your credit score, income, the size of your deposit, the property type, and how you are employed all affect which lenders will offer you their best rates. A lender that is perfect for one buyer might not even approve another.

Research from Freddie Mac found that homebuyers who obtained just two quotes saved over £1,500 over the life of their loan. Those who got five quotes saved around £3,000. The more you compare, the more you are likely to save.

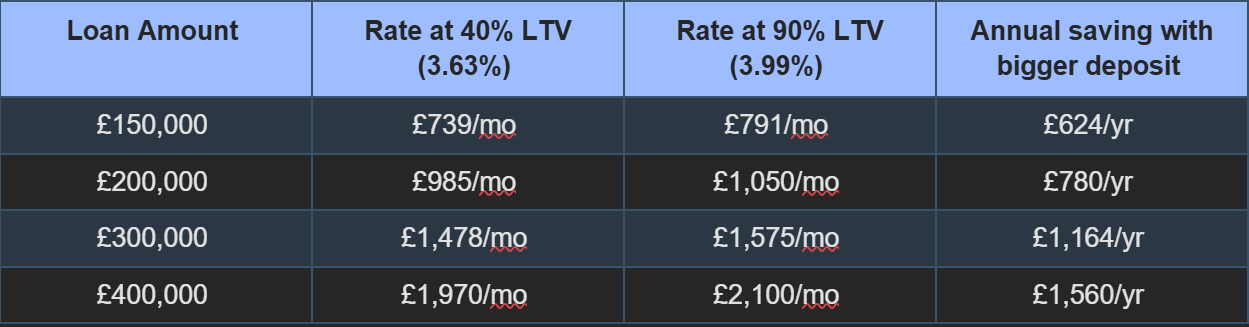

One of the biggest factors that determines your mortgage rate is your loan-to-value ratio, or LTV. This is the percentage of the property's value you are borrowing.

Simply put: the more you put down, the lower your rate. Here is how the numbers stack up:

Even moving from a 10% deposit to a 25% deposit can make a noticeable difference to your monthly payment. If you are a first-time buyer and struggling to save a larger deposit, do not worry. There are still good rates available at 90% LTV, and a mortgage broker can help you find lenders who are most competitive at that level.

This is one of the most common questions first-time buyers ask. Here is a plain-English explanation of the main types:

You pay the same interest rate for a set period, usually 2, 3, 5 or 10 years. Your monthly payment stays the same regardless of what happens to interest rates elsewhere. This is great for budgeting and gives you certainty.

The trade-off is that if rates fall significantly during your fixed term, you will not benefit until your deal ends.

Your rate moves up and down in line with the Bank of England base rate. If the base rate goes down, so do your payments. If it goes up, your payments rise too. Trackers can be good value if rates are expected to fall, but they add uncertainty to your monthly budget.

This is the rate your lender puts you on when your fixed or tracker deal ends. It is set by the lender, not the Bank of England, and it is almost always the most expensive option. The average SVR in March 2026 is 7.15%. Unless you have a specific reason to be on it, you should look to remortgage before landing on your lender's SVR.

With rates expected to potentially ease over 2026, a 2-year fixed deal gives you security in the short term while keeping your options open sooner. A 5-year fix offers more certainty if you want to lock in today's rate and not worry about it for longer. The right answer depends on your personal circumstances, which is exactly the kind of question a good mortgage broker will help you think through.

Here is exactly what you should do to make sure you get the best deal available to you.

Lenders use your credit score to decide whether to lend to you and at what rate. A higher score usually means a lower rate. Check your score for free through services like Experian, Equifax or Credit Karma before you apply. If there are any errors, get them corrected. Even paying off a small outstanding debt can improve your score before application.

Divide the amount you want to borrow by the property's value and multiply by 100. The lower this number, the better. Rates improve significantly at 90%, 75% and 60% LTV, so if you can stretch your deposit to hit one of those thresholds, it is worth doing.

Do not go straight to your own bank and accept whatever they offer. Your bank has no obligation to give you their best rate, and they are just one of many lenders out there. Comparing multiple lenders could save you a meaningful amount of money every month.

A whole-of-market broker, like Mortgage Brokers Near Me, can access deals from over 90 lenders including some that are not available directly to the public. They will also know which lenders are most likely to approve your particular financial situation, which saves you applying in the wrong places and getting unnecessary credit checks on your file.

Importantly, a fee-free broker earns their fee from the lender rather than from you, so this service costs you nothing.

You can agree a mortgage rate up to 6 months before you need it. Given that rates are starting to tick upwards in March 2026, locking in a rate now and keeping it under review is a sensible strategy. If rates improve before you complete, a good broker will help you switch to a better deal.

Some mortgages come with arrangement fees of £1,000 or more. A mortgage with a slightly higher rate but no fee can actually be cheaper overall, depending on your loan size and term. Always compare the overall cost of the deal, which is captured in the APRC (Annual Percentage Rate of Charge).

This is a question we hear all the time. The honest answer is that trying to time the mortgage market is very difficult, and in most cases waiting costs more than it saves.

Greg Schwartz, CEO of Tomo Mortgage, put it well: if you find the right home and can afford the monthly payments, you should take the opportunity. If rates decline later, competition from other buyers increases, sellers regain leverage, and prices tend to follow.

In simple terms: lower rates often lead to higher house prices. The saving on your mortgage rate can get cancelled out by paying more for the property.

If you are buying to live in the property for the long term, and the monthly payment is affordable for you today, waiting for a perfect rate is rarely the right strategy.

If rates do fall after you take out your mortgage, you can remortgage to a better deal when your fixed term ends. You are not locked in forever.

If your current mortgage deal is coming to an end, or if you are on your lender's SVR already, remortgaging could save you a significant amount of money every month.

Here is when you should start looking:

One option worth asking about is a rate lock with a float-down clause. This lets you secure a rate today but switch to a lower one if rates fall before you complete. Not every lender offers this, but a broker can help you find one that does.

Mortgage Brokers Near Me is a UK-based, FCA-regulated mortgage advisory service. We work with first-time buyers, home movers and people looking to remortgage, and we have access to deals from over 90 lenders across the market.

Getting a mortgage is not just about finding the lowest number. It is about finding the right deal for your situation: the right term, the right type of rate, the right lender for your credit profile. That is what a good mortgage broker does.

If you are ready to find out what rate you could get today, get in touch with Mortgage Brokers Near Me for a free, no-obligation conversation.

A good mortgage rate in 2026 depends on your deposit size and credit profile. As a general guide, rates below 4% on a 2-year fixed deal are considered competitive for buyers with a 25% or larger deposit. For 90% LTV (10% deposit), rates of under 4.20% are strong. Always compare multiple lenders to make sure you are getting the best deal available to you.

The average 2-year fixed mortgage rate in the UK as of early March 2026 is approximately 4.30%, according to Rightmove. The average 5-year fixed rate is around 4.44%. However, the best available rates are lower than these averages, which is why comparing lenders and using a broker matters.

You can get a mortgage with as little as a 5% deposit, though rates are higher at that level. The main rate improvements come at 10%, 25% and 40% deposit. A 40% deposit typically gives you access to the lowest rates on the market. Most first-time buyers aim for at least 10% as a starting point.

LTV stands for loan-to-value. It tells you what percentage of the property's value you are borrowing. For example, if you want to buy a £250,000 property and have a £25,000 deposit, you are borrowing £225,000, which is 90% of the property's value. That is 90% LTV. The lower your LTV, the better your mortgage rate will generally be.

A mortgage rate lock is when a lender agrees to hold a specific interest rate for you for a set period, usually until you complete your purchase or remortgage. This protects you if rates rise before you complete. In the UK, you can typically lock in a rate up to 6 months before your completion date. Some lenders offer a float-down option, which lets you benefit if rates fall before you complete.

Given that mortgage rates have started to rise in March 2026 due to global uncertainty, locking in a rate as soon as you are serious about buying or remortgaging is sensible. Do not wait for rates to fall to a specific level, as this is very difficult to predict and waiting often means missing good deals.

Your mortgage interest rate is the rate used to calculate your monthly payment. The APRC (Annual Percentage Rate of Charge) is a broader figure that includes the interest rate plus any fees spread over the full term of the mortgage. When comparing deals, always look at the APRC to understand the true total cost.

When your fixed rate period ends, you automatically move on to your lender's Standard Variable Rate (SVR) unless you arrange a new deal. The average SVR in March 2026 is 7.15%, which is significantly higher than current fixed rates. To avoid this, start comparing new deals at least 3 months before your current deal ends, ideally 6 months ahead.

Using a whole-of-market mortgage broker gives you access to a wider range of deals, including some not available directly to the public. A broker can also help identify which lenders are most likely to approve your application based on your financial situation. For most people, using a broker results in a better rate and a smoother process than going direct.

The short-term direction is slightly upwards in March 2026, as lenders react to global events pushing up inflation expectations. However, the overall trend for 2026 is expected to be broadly stable with the possibility of gradual eases later in the year if inflation continues to fall. Nobody can predict rates with certainty, which is why acting when you find a rate you can afford makes more sense than waiting.

Is It Worth Going Through a Mortgage Broker? A Complete Guide for Homebuyers in Reading

Read Article

Discover how assumable mortgages work, which loan types qualify, and the pros and cons of assuming a mortgage. Learn how this strategy could save you money in a high-rate market – and how Mortgage Broker Near Me can help you make it happen.

Read Article

A clear, real-world breakdown of how much you need to earn to buy a £250,000 home in the UK. This guide explains how lenders calculate affordability, how deposit size affects borrowing, what monthly repayments typically look like, and why location plays a huge role in what £250,000 can buy. Written to help first-time buyers sense-check the numbers before making an offer.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR