Mortgage rates in 2026 are rising quickly due to global instability and “Trumpflation,” with lenders pulling deals and increasing rates in real time. Sub-4% mortgages are disappearing, and borrowing costs are climbing faster than many expected. For buyers and homeowners, waiting could mean higher monthly payments and fewer options. The safest move right now is to compare lenders early and secure a deal before rates move again.

Mar 19, 2026

In just a matter of weeks, lenders have pulled hundreds of mortgage deals, sub-4% rates have almost disappeared, and average fixed rates have jumped again. For many borrowers, that shift has already added hundreds of pounds a year to the cost of a new mortgage.

If you’re buying or remortgaging, this isn’t background noise. It directly affects what you’ll pay every month.

The bigger problem is how fast things are changing. This isn’t a slow trend. It’s happening in real time.

Over a short period, mortgage pricing has shifted sharply.

Average fixed rates have climbed back above 5%, reversing the downward trend many people were expecting. At the same time, lenders have been withdrawing products and repricing aggressively.

That combination matters more than the headline rate itself.

When lenders pull deals, your choice shrinks. When rates rise at the same time, you’re not just paying more, you’re picking from a smaller pool of options.

This is exactly the kind of market where borrowers get caught out. They assume things will settle, wait a few weeks, and come back to find the deal they wanted has gone.

Mortgage rates were supposed to be settling in 2026. Instead, they’ve moved in the opposite direction and quickly.

In just a matter of weeks, lenders have pulled hundreds of mortgage deals, sub-4% rates have almost disappeared, and average fixed rates have jumped again. For many borrowers, that shift has already added hundreds of pounds a year to the cost of a new mortgage.

If you’re buying or remortgaging, this isn’t background noise. It directly affects what you’ll pay every month.

The bigger problem is how fast things are changing. This isn’t a slow trend. It’s happening in real time.

Over a short period, mortgage pricing has shifted sharply.

Average fixed rates have climbed back above 5%, reversing the downward trend many people were expecting. At the same time, lenders have been withdrawing products and repricing aggressively.

That combination matters more than the headline rate itself.

When lenders pull deals, your choice shrinks. When rates rise at the same time, you’re not just paying more, you’re picking from a smaller pool of options.

This is exactly the kind of market where borrowers get caught out. They assume things will settle, wait a few weeks, and come back to find the deal they wanted has gone.

Mortgage rates don’t move randomly. They’re driven by what’s happening in the wider economy.

Right now, a mix of global uncertainty, rising energy costs, and inflation concerns has pushed up the cost for lenders to fund mortgages. When those costs rise, lenders pass it on.

That’s why you’re seeing:

It’s not about one lender making a change. It’s happening across the market at the same time.

And once that cycle starts, it tends to move faster than people expect.

If you’re buying your first home or moving, your affordability is changing in real time.

A rate increase of even 0.3% might not sound like much, but it can mean a noticeable jump in monthly payments. Stretch that over a 25 or 30-year mortgage and the cost difference becomes serious.

The bigger issue is uncertainty.

You could agree a purchase based on one set of numbers, only for rates to move before you secure your mortgage. That leaves you either paying more or having to rethink your budget entirely.

This is why waiting for “perfect timing” doesn’t work in practice. The market doesn’t pause while you decide.

This is where it hits hardest.

A large number of borrowers are coming off fixed deals in 2026. Many of those deals were taken out when rates were significantly lower.

If you’re in that position, the jump you’ll see isn’t small. It can be a sharp increase in monthly cost.

On top of that, if you do nothing, you risk falling onto your lender’s standard variable rate. That’s usually far higher than any fixed deal available.

The key point here is timing.

You don’t need to wait until your current deal ends. In most cases, you can start looking at new rates months in advance and secure something before things move further.

Leaving it late removes that option.

A lot of people are holding off right now, hoping rates will drop again.

On paper, that sounds sensible. In reality, it’s risky.

Mortgage pricing doesn’t move in a straight line. Rates can rise quickly, and the best deals can disappear overnight. Even if rates improve later, there’s no guarantee the products you need will be available when you come to apply.

What tends to happen is this:

Trying to time the market perfectly usually backfires.

A better approach is to secure a deal that works now and keep your options open where possible.

Not all lenders react the same way.

Some increase rates faster. Some hold pricing longer. Some target specific types of borrowers. Others quietly become uncompetitive.

That means the gap between lenders widens when the market is unstable.

If you only check one bank, you’re guessing. You have no idea whether that deal is actually competitive or just convenient.

Comparing lenders properly isn’t about chasing the lowest headline rate. It’s about:

This is where most people either save money or lose it.

You don’t control the market, but you can control how you respond to it.

Start by getting a clear view of your options early. If you’re remortgaging, don’t leave it until the last minute. If you’re buying, understand what rates look like before you commit.

Make sure you’re not focusing on rate alone. Fees, flexibility and timing all matter just as much.

Most importantly, don’t assume today’s deals will still be there next week.

Because right now, they often aren’t.

At Mortgage Brokers Near Me, we’ve been helping clients secure competitive interest rates by comparing lenders across the whole market, not just one bank.

We look at:

This matters more in a market like this, where the difference between lenders can change quickly.

Get in touch with MBNM today and we’ll help you compare your options properly and secure the best rate available to you.

Because in this market, the people who move early usually end up in a better position than those who wait.

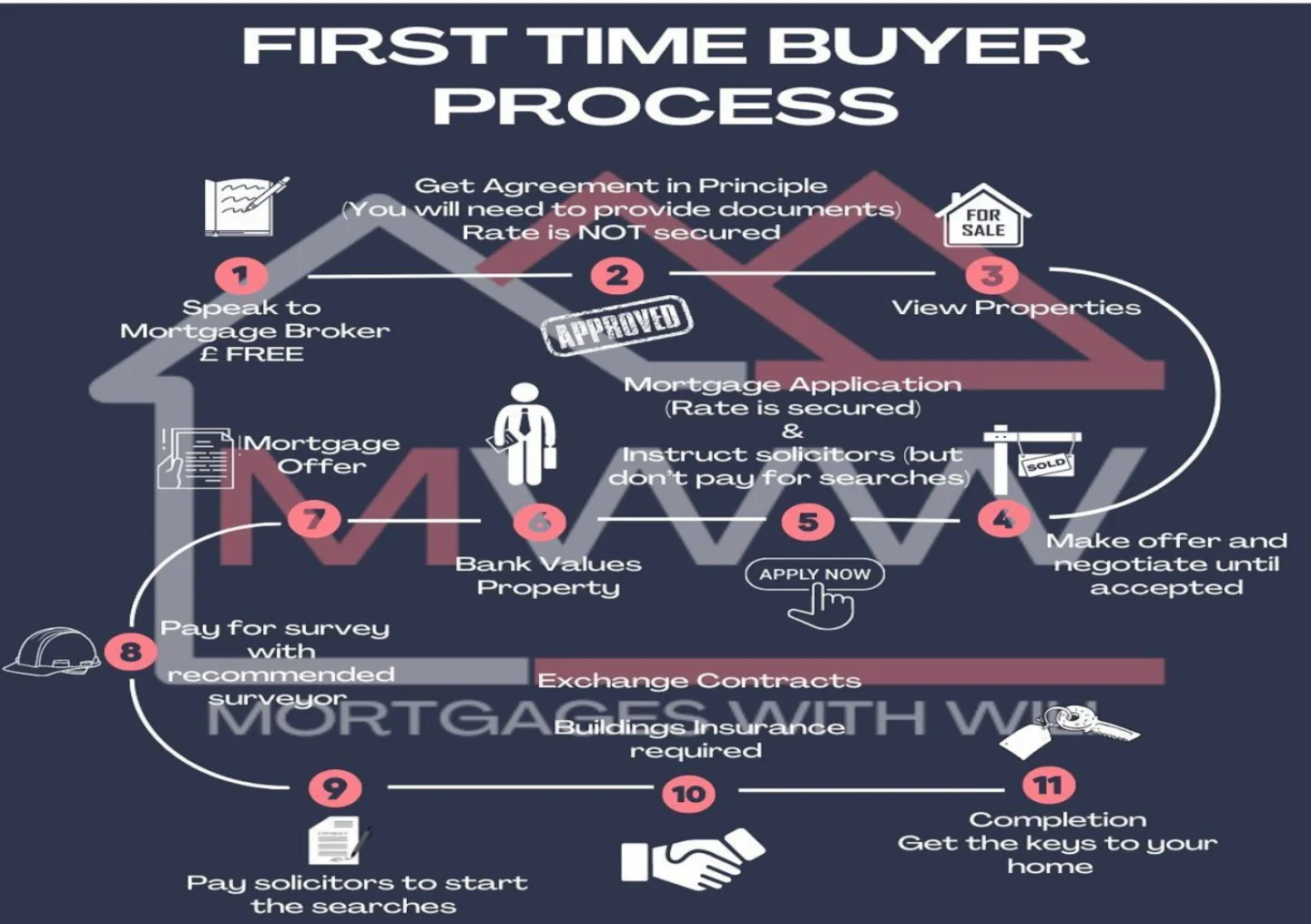

A clear, step-by-step guide to the first-time buyer process, written by Will Sharman of Mortgage Brokers Near Me. Learn what happens at each stage and when to get expert help.

Read Article

Is Using a Mortgage Broker Worth It? A Complete Guide for Homebuyers in Essex

Read Article

Should I Use a Mortgage Broker? A Complete Guide for Homebuyers in London

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR