Can I get a joint mortgage with an IVA? Yes – but it depends on the IVA’s status, your deposit size, and your partner’s credit profile. This guide from Will Sharman at Mortgage Brokers Near Me explains how joint mortgages work with an IVA, which lenders might accept you, and what to expect during the process. Includes FAQs, real-life examples, and expert tips to boost your approval chances.

Jul 7, 2025

A joint mortgage is when two or more people apply for a mortgage together – often partners, family members, or friends. But if one person has a financial history that includes an IVA (Individual Voluntary Arrangement), it’s natural to wonder if you’ll still be eligible to get approved.

Good news: Yes, it is possible to get a joint mortgage if one of you has an IVA – but it’s more complex than a standard application. Let’s break it all down.

An IVA is a formal debt solution that helps people pay back a portion of what they owe through affordable monthly payments. It usually lasts five to six years, and stays on your credit file for six years from the date it begins.

Because it’s listed on your credit history, mortgage lenders see it as a red flag – but that doesn’t mean automatic rejection.

“With more than 75,000 IVAs approved in the UK last year, we’re seeing a steady rise in joint mortgage enquiries where one partner has an IVA. Lenders are adapting but deposit size and timing still matter.” — Will Sharman,

Yes, you can – but the lender will look at both applicants’ credit profiles, and usually base their decision on the weaker of the two.

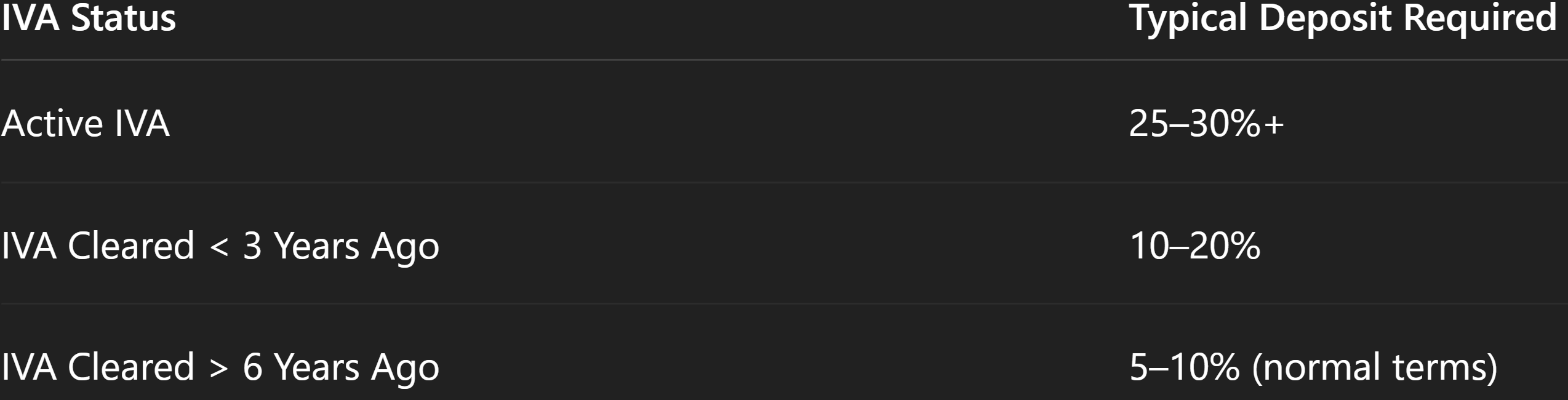

Yes – deposit size matters more when an IVA is involved.

The bigger the gap since your IVA was cleared, the better the deal you’re likely to get.

Is it still active or fully discharged? The longer it’s been cleared, the better your options.

Lenders will assess whether you can still afford the mortgage payments, especially if you're still repaying debts under an IVA.

They’ll check payment history, defaults, and whether you've been rebuilding credit.

Lenders reduce their risk by requiring a higher deposit. LTV caps may be lower for applicants with an IVA.

This is sometimes possible – but it’s not always the best move.

Speak to a broker to run both scenarios before deciding.

Yes, but you’ll likely need a bigger deposit and a specialist lender. Expect the lender to base their decision on the person with the IVA.

Yes. Always be transparent. Lenders will find it in credit checks, even if it’s off your file.

Yes, but only with certain lenders – and only if the IVA is cleared before completion. We can help you check the latest scheme rules.

Absolutely. Once you pass the 3- or 6-year mark, many high-street lenders will offer improved rates and lower deposit requirements.

“Most mainstream lenders won’t accept IVA applicants, but the specialist mortgage market in 2025 is far more flexible than it was just a few years ago. With the right prep, approval is absolutely possible.” — Will Sharman, Mortgage Broker

A lot of people try to go it alone or apply with their bank – only to get declined and damage their credit file further. Don’t make that mistake.

Get a free quote or personalised mortgage check today Let’s find out if now’s the right time and if not, we’ll show you exactly what to do to get ready.

Using a mortgage broker usually makes sense if your situation isn’t completely straightforward, for example if you’re self-employed, have credit history, are buying for the first time, or simply don’t want to risk choosing the wrong lender. A broker can match you to lenders that fit your case and handle the application process. Going direct to a bank can work if your income, deposit and credit profile are simple and you’re confident comparing products yourself. If you’re unsure, speak to a broker first. At MBNM, the first chat is free and we can help you secure a Mortgage in Principle so you know exactly where you stand before moving forward.

Read Article

Right to Buy and Right to Acquire are often confused, but they are not the same scheme. Right to Buy usually applies to council tenants and offers larger discounts, while Right to Acquire applies to many housing association tenants and comes with smaller, fixed discounts. The mortgage rules, lender appetite, and deposit expectations can differ, so knowing which scheme applies to you before applying for a mortgage matters more than most people realise.

Read ArticleWith interest rates shifting and remortgage deals changing weekly, choosing between a fixed or tracker mortgage in 2025 isn’t just about the numbers, it’s about what fits your goals, budget, and risk tolerance. In this guide, we break down the pros and cons of both options, share real examples from clients we've helped, and give you the insight you need to make the right move this year.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR