Tenure explains how you legally own a property. Freehold means you own the building and the land outright. Leasehold means you own the property for a fixed period but not the land. The difference affects mortgage eligibility, resale value and long-term costs. If you are buying or remortgaging, tenure is not just legal jargon. Lenders care about it. A short lease, ground rent clauses or restrictive terms can limit which lenders will consider your application. This guide explains what tenure means in plain English and how it affects your mortgage.

Feb 16, 2026

.webp)

Tenure is the legal way in which a property is owned.

In England and Wales, the main types of tenure are:

Each type gives you different rights, responsibilities and costs.

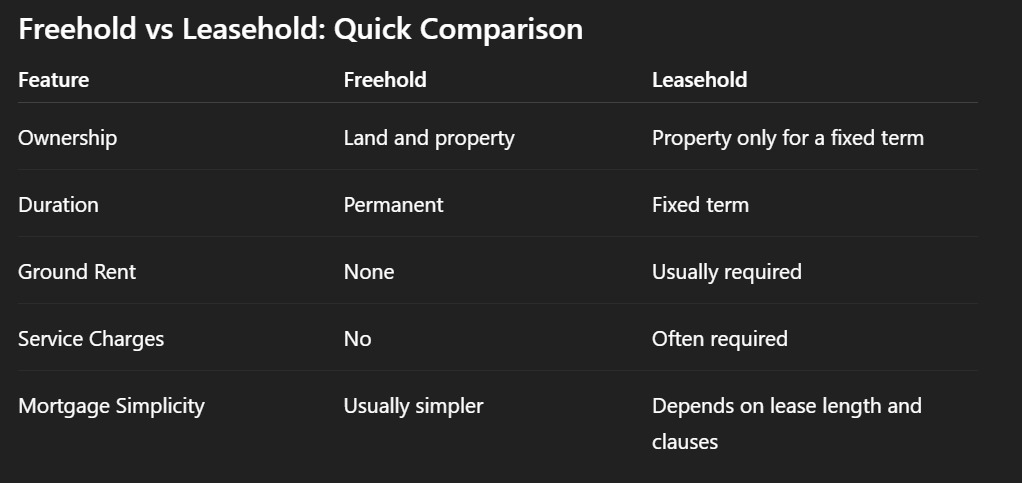

Freehold means you own the property and the land it stands on indefinitely. There is no expiry date.

If you buy a freehold property:

Most houses in England and Wales are freehold. Some flats and new-build houses can also be freehold, but this is less common.

From a mortgage perspective, freehold is usually straightforward.

There is:

This often means broader lender choice and smoother underwriting.

Leasehold means you own the property for a fixed number of years under a legal agreement called a lease. You do not own the land.

When the lease ends, ownership returns to the freeholder unless it is extended.

Typical lease lengths range from 90 to 999 years when first granted.

Most flats are leasehold. Some houses, particularly on modern estates, can also be leasehold.

If you buy leasehold, you may need to pay:

You may also need permission for structural changes or sub-letting.

This is where things get serious for buyers.

Lenders have minimum lease length requirements.

Here is a general guide:

85+ years remaining:

Strong lender appetite. Most mainstream lenders are comfortable.

70–85 years remaining:

Mixed appetite. Some lenders accept. Others require confirmation that the lease will be extended.

Below 70 years remaining:

Many mainstream lenders decline. Specialist solutions may be required.

Below 80 years, lease extensions become more expensive because of marriage value. That can affect both affordability and resale value.

If you are unsure about lease length, check the title early. Do not leave it until after your offer is accepted.

Ground rent and service charges can affect affordability calculations.

Lenders will review:

Some lenders are cautious about aggressive ground rent escalation clauses. Others require specific wording to be present in the lease.

This is why tenure is not just academic. It directly impacts your mortgage options.

Commonhold is less common but growing.

Under commonhold:

There is no traditional landlord.

From a lending perspective, commonhold can be acceptable, but availability varies between lenders.

Buyers sometimes discover a lease under 75 years after agreeing a price. This can reduce lender choice and increase costs.

Leaseholders collectively own the freehold. This can improve control but still requires careful review of the lease terms.

Some lenders require minimum lease terms at completion and restrict certain ground rent structures.

Sub-letting clauses and insurance obligations must align with lender policy.

These details matter. Overlooking them can lead to delays or declined applications.

The right advice early can mean:

As mortgage advisers, we check tenure and lease length at the start, not halfway through.

We review:

That avoids wasted applications and unnecessary stress.

Not necessarily. Many perfectly good properties are leasehold. The key factors are lease length, ground rent terms and service charge levels.

Yes, provided it meets lender criteria. Lease length and clauses are the main considerations.

Ownership reverts to the freeholder unless extended. Most leaseholders extend long before expiry.

Freehold offers more control and fewer ongoing charges. But suitability depends on property type and personal circumstances.

If you are unsure whether a property’s tenure could affect your mortgage, speak to us before committing.

We will explain your options clearly and check lender criteria early in the process.

Book a free appointment today.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Ground rents are being capped at £250 a year, but the change is not immediate and it does not automatically fix mortgage issues for leaseholders. This guide explains what ground rent is, what the new cap actually means, when it comes into force, and how lenders assess leasehold properties today. Written to help buyers and existing leaseholders avoid costly mistakes when selling, buying, or remortgaging a leasehold home.

Read Article

Using a mortgage broker usually makes sense if your situation isn’t completely straightforward, for example if you’re self-employed, have credit history, are buying for the first time, or simply don’t want to risk choosing the wrong lender. A broker can match you to lenders that fit your case and handle the application process. Going direct to a bank can work if your income, deposit and credit profile are simple and you’re confident comparing products yourself. If you’re unsure, speak to a broker first. At MBNM, the first chat is free and we can help you secure a Mortgage in Principle so you know exactly where you stand before moving forward.

Read Article

Freehold usually means fewer moving parts, you own the building and the land, you handle maintenance, and there’s no ground rent or service charges. Leasehold means you own the property for a set number of years, and the building (and land) is owned by a freeholder, so you may pay service charges and ground rent, and you can be restricted by the lease. For mortgages, the big “gotcha” is lease length. Once a lease starts getting short (especially heading towards 80 years), it can affect value and lender options, and extending later can get expensive. Reforms are in motion in England and Wales, but you still need to buy based on today’s rules, not headlines.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR