Considering a remortgage in 2025? This guide breaks down fixed vs tracker mortgages in plain English - with real examples, expert advice, and a clear path to choosing the right deal for your situation.

Jun 30, 2025

When it comes to getting a mortgage in 2025, most people are asking:

“Should I go direct to a bank or use a mortgage broker?”

And more importantly:

“Which one will actually get me the best deal?”

In this guide, we’ll break it down simply. Just real answers from years of experience helping people like you at Mortgage Brokers Near Me.

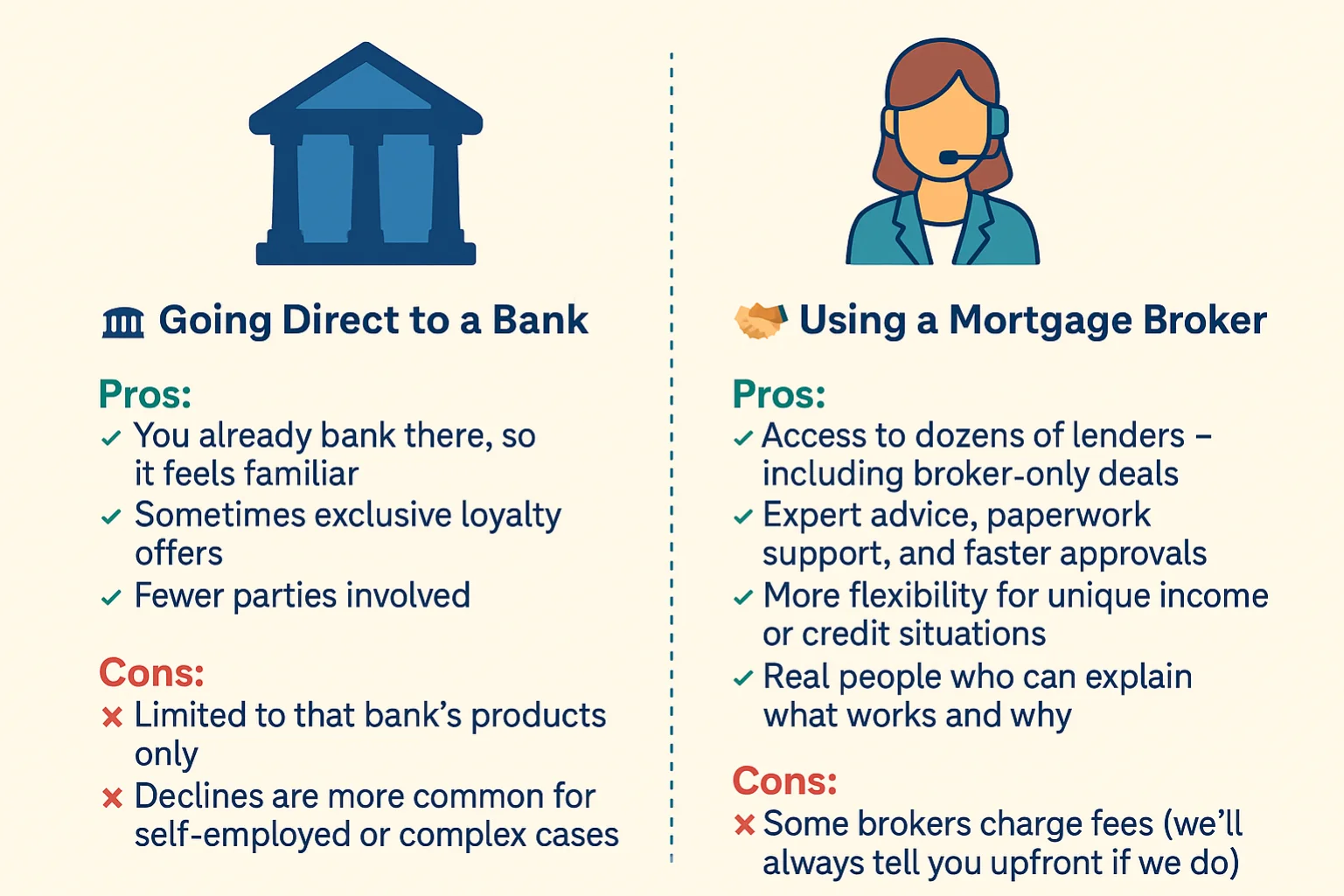

A bank offers you mortgage products from their own internal range. That means:

A broker works across many lenders to find the best deal for your situation. Brokers:

→ Use a broker. Most banks have strict criteria and may reject applications that don’t fit a perfect mould. Brokers know which lenders are flexible.

→ Use a broker. They can access specialist lenders with better 90–95% LTV options.

→ Try your bank too. It’s worth checking what they can offer just don’t stop there.

→ Go broker. Banks sell their own deals. Brokers give tailored guidance based on your goals, not just their product list.

"We speak to clients every week who’ve gone straight to their bank, been declined, and didn’t realise there were better options out there. A broker’s job isn’t to sell it’s to guide you to what actually works for your situation."

Not always. Some are free (paid by the lender), while others charge a fee.

But often, brokers can still save you more money than you'd pay in fees.

✅ At Mortgage Brokers Near Me, we’ll tell you upfront if it’s worth it or not.

Banks = more admin on you.

Brokers = one conversation → 30+ lender comparisons handled for you.

Banks = 1 lender’s deals

Brokers = 30–100+ lenders, including broker-only products

Tom came to us after being declined by his bank due to inconsistent income.

We matched him with a specialist lender who approved his mortgage at 85% LTV with a competitive fixed rate saving him the stress of applying again and risking his credit score.

Emily had a 5% deposit and was told by her bank that she’d need to wait longer.

We secured her a mortgage with a broker-only lender who accepted her on the same day not

A: Often, yes. They can access exclusive or specialist rates that banks don’t offer direct.

A: Yes. UK mortgage brokers are regulated by the FCA and legally must act in your best interest.

A: Not always. Many are free, or their fee is offset by a better deal. We’ll tell you upfront.

A: Absolutely. It’s one of the most common reasons people come to us.

At Mortgage Brokers Near Me, we:

Will Sharman has over 10 years of experience helping buyers, self-employed clients, and remortgagers find the right deal even in complex or urgent situations.

"I thought my bank would give me the best deal because I’ve been with them for years but Will found me a better rate with another lender and handled everything start to finish."

Whether you’re comparing deals, remortgaging, or buying your first home we’ll help you find out what you really qualify for, not just what a bank tells you.

Book a free call now with Will or one of our brokers we’ll do the legwork, show you your best options, and help you move forward with confidence.

Many homeowners are stuck on expensive rates or rejected for remortgages. Most of the time it’s not because they can’t afford it, but because they don’t know how lenders actually judge affordability in 2025. This guide breaks down the main reasons applications get blocked, and how a broker helps you get unstuck fast.

Read Article

Is Using a Mortgage Broker Worth It? A Complete Guide for Homebuyers in Essex

Read Article

If you’re a council tenant wondering whether you need a deposit to buy your home, the answer is often no. With the Right to Buy scheme, many lenders allow the council discount to be used as your deposit, meaning you can purchase your property without putting down cash savings. While affordability, credit history, and property type still matter, the right advice can make the difference between thinking homeownership is out of reach and actually making it happen.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR