Discover how assumable mortgages work, which loan types qualify, and the pros and cons of assuming a mortgage. Learn how this strategy could save you money in a high-rate market – and how Mortgage Broker Near Me can help you make it happen.

Apr 11, 2025

Buying a home can be tricky enough without worrying about rising interest rates. But what if there was a way to take over someone else's lower-rate mortgage? That’s where assumable mortgages come in. Let’s break it down in simple terms.

An assumable mortgage lets a homebuyer take over the seller’s existing mortgage — including the interest rate, loan balance, and terms. It’s like stepping into their shoes and picking up where they left off.

This can be a major win for buyers, especially if the seller locked in a low interest rate when the market was better.

Not all loans are created equal. Here’s a quick look at which ones can be assumed:

“Comparison sites show you options. Mortgage brokers show you what’s right for you — based on your goals, not just the rates.”

In most cases, no. These usually come with a “due-on-sale” clause — meaning the mortgage must be paid in full when the home is sold. Some adjustable-rate mortgages (ARMs) might be assumable, but it’s rare and lender-specific.

Check the seller’s loan paperwork or ask their lender to confirm if the mortgage can be assumed.

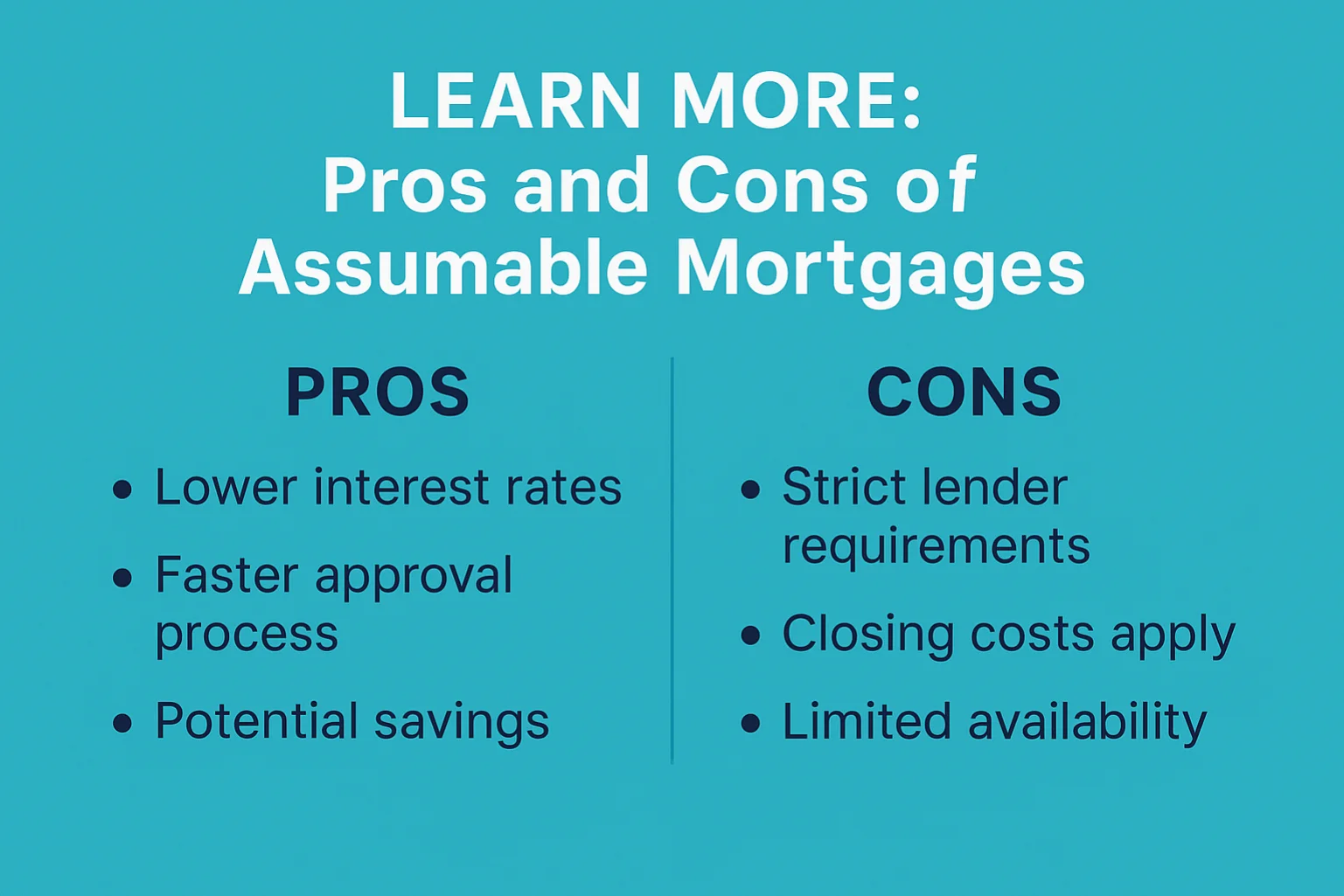

Even if the loan is assumable, the buyer usually needs to qualify — similar to applying for a new loan.

You’ll need to pay the seller whatever equity they’ve built up in the home. For example, if the house is worth £300,000 and the mortgage has a balance of £200,000, you may need to cover the remaining £100,000 upfront or via a second loan.

After approval, sign the paperwork, pay any fees, and officially assume the mortgage.

Yes. In cases of death or divorce, mortgages can sometimes be assumed without going through the standard application. You may still need to cover equity and other legal steps.

Costs can vary, but typically include:

You need to meet the lender’s credit and income requirements, similar to a new mortgage.

Not in the traditional sense, but you’ll need to cover the seller’s equity somehow — either from savings or another loan.

Not always. If you assume an FHA loan, for example, you’ll still need to pay mortgage insurance.

They’re not super common, but they’re becoming more popular as interest rates stay high.

“A good mortgage broker doesn’t just find you a deal — they save you hours of paperwork, weeks of waiting, and thousands over the term.”

At Mortgage Broker Near Me, we help buyers and sellers navigate the complex world of home financing. Whether you’re looking to assume a mortgage or just want to explore your options, our expert advisors are here to make the process easier and clearer. We’ll:

Want to save thousands over the life of your loan? Start your journey with us today.

Assumable mortgages might not be the most common route, but in the right situation, they can be a smart way to save on interest and make a home more affordable. As always, work with a trusted mortgage broker to explore all your options and decide what’s right for you.

Need help finding or assuming a mortgage? Get in touch with our team at Mortgage Broker Near Me today.

Ground rents are being capped at £250 a year, but the change is not immediate and it does not automatically fix mortgage issues for leaseholders. This guide explains what ground rent is, what the new cap actually means, when it comes into force, and how lenders assess leasehold properties today. Written to help buyers and existing leaseholders avoid costly mistakes when selling, buying, or remortgaging a leasehold home.

Read Article

Using a mortgage broker usually makes sense if your situation isn’t completely straightforward, for example if you’re self-employed, have credit history, are buying for the first time, or simply don’t want to risk choosing the wrong lender. A broker can match you to lenders that fit your case and handle the application process. Going direct to a bank can work if your income, deposit and credit profile are simple and you’re confident comparing products yourself. If you’re unsure, speak to a broker first. At MBNM, the first chat is free and we can help you secure a Mortgage in Principle so you know exactly where you stand before moving forward.

Read Article

Life insurance in your 20s can be a smart move, but not for everyone. If nobody depends on you financially, it may not need to be top of your list yet. But if you have a partner, children, a mortgage, or shared financial commitments, it can be worth putting cover in place earlier while it is often cheaper and easier to arrange.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR