Should I Use a Mortgage Broker? A Complete Guide for Homebuyers in Milton Keynes

Mar 18, 2025

Buying a home or remortgaging is one of the biggest financial decisions you’ll make. If you’re wondering “Should I use a mortgage broker?”, you’re not alone. Many people in Milton Keynes are unsure whether to go directly to a bank or work with a mortgage broker.

At Mortgage Brokers Near Me, we specialize in providing expert mortgage advice, helping homebuyers and homeowners find the best mortgage deals. This guide will cover:

✅ Which bank is easiest to get a mortgage with in the UK?

✅ Should I get a mortgage broker or do it myself?

✅ What is a red flag in a mortgage?

✅ Do lenders look at spending habits?

✅ How to get the lowest mortgage rate?

✅ Can I get free mortgage advice?

Let’s break it all down.

A mortgage broker is a financial expert who searches for the best mortgage deals on your behalf. Instead of applying to different banks yourself, a broker:

Searches the market to find the lowest interest rates.

Handles paperwork to streamline the mortgage process.

Provides expert advice tailored to your financial situation.

Helps you save money by finding the best mortgage rates.

Unlike banks, mortgage brokers aren’t tied to one lender, meaning they offer unbiased advice and access to a wider range of mortgage products.

“A good mortgage broker doesn’t just find you a deal — they save you hours of paperwork, weeks of waiting, and thousands over the term.”

Some banks are known for easier mortgage approvals, especially for first-time buyers or self-employed applicants. Here are a few top choices:

🏦 Halifax – Great for first-time buyers and offers flexible lending criteria.

🏦 Barclays – Strong buy-to-let and first-time buyer mortgage options.

🏦 Nationwide – Known for low deposit mortgages and great remortgage deals.

🏦 HSBC – Offers competitive mortgage rates for professionals and high earners.

🏦 NatWest – Has mortgage advisors and flexible options for various income levels.

Each bank has different lending criteria, so working with a mortgage broker can help match you to the best lender for your financial profile.

Yes! Lenders analyze your bank statements to assess:

Regular monthly expenses – Bills, rent, subscriptions, and discretionary spending.

Savings habits – Having money saved shows financial responsibility.

High-risk spending – Gambling transactions or excessive shopping may raise red flags.

Large unexplained transactions – Lenders want a clear picture of your financial situation.

💡 Tip: Before applying, review your bank statements for the last 6 months and reduce unnecessary spending.

If your mortgage payments feel too high, here are ways to reduce them:

Remortgage – Switch to a lower interest rate.

Increase Your Deposit – A larger deposit reduces monthly payments.

Extend Your Mortgage Term – Spreading payments over 30+ years can lower monthly costs.

Pay Off Other Debts – Reducing your debt-to-income ratio can help qualify for lower rates.

A mortgage broker can help find the best refinancing options to cut your monthly payments.

Securing the lowest mortgage rate can save you thousands over the term of your loan. Here’s how to get the best deal:

🔹 Improve Your Credit Score – Higher scores get lower rates.

🔹 Increase Your Deposit – A bigger deposit means lower interest rates.

🔹 Compare Lenders – Banks only offer their own rates, while brokers compare 90+ lenders.

🔹 Opt for a Fixed Rate Mortgage – Locks in a low rate for 2-5 years.

🔹 Reduce Your Debt-to-Income Ratio – Pay down credit cards and loans before applying.

A mortgage broker will find the lowest rate based on your situation, ensuring you don’t overpay on interest.

“I have no debt” – If you have credit cards or loans, be upfront about them.

"just changed jobs” – Lenders prefer stable employment before approving a mortgage.

“I can afford more than my budget” – Banks assess affordability based on income, not personal estimates.

“I’m planning a big purchase soon” – Large expenses before your mortgage approval can reduce your borrowing power.

Being honest about your financial history helps brokers find the best mortgage deal for you.

Yes! Many mortgage brokers, including Mortgage Brokers Near Me, offer free, no-obligation mortgage advice. Some brokers earn commission from lenders, meaning their service is free to you.

✅ Independent mortgage advice tailored to your needs.

✅ Expert guidance without hidden fees.

✅ Access to better rates than banks offer directly.

If you’re looking for free mortgage advice in Milton Keynes, contact us today to explore your options.

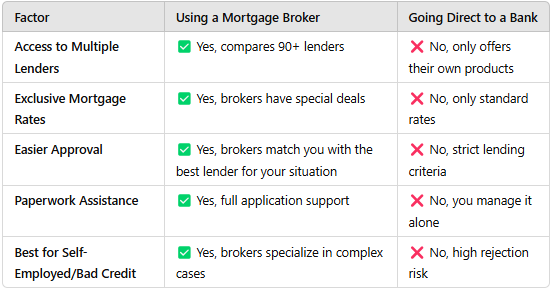

Many buyers ask, “Should I use a mortgage broker or go directly to a bank?” Here’s a quick comparison below.

Using a mortgage broker gives you access to better mortgage rates, easier approval, and professional support—all at no extra cost in many cases.

“Comparison sites show you options. Mortgage brokers show you what’s right for you — based on your goals, not just the rates.”

If you want the best mortgage rates, expert advice, and an easy application process, using a mortgage broker in Milton Keynes is the right choice.

✔ Find the lowest interest rates

✔ Compare mortgages from 90+ lenders

✔ Get free, expert mortgage advice

✔ Increase your chances of approval

📞 Get in touch today and start your mortgage journey with confidence!

Mortgage rates have steadied after months of change, but affordability is still tight. The Bank of England hasn’t moved the base rate yet, and talk of a new property tax has made some buyers nervous. If you’re thinking about buying or remortgaging, the best move right now is to plan early, get advice, and focus on what you can control, not the headlines.

Read Article

Mortgage rates in 2026 could drift lower, but expecting a clean, straight-line drop is wishful thinking. Lenders price in expectations early, inflation surprises still move markets fast, and your “best” move depends more on your deal end date, your deposit or equity, and your risk tolerance than on any headline forecast.

Read Article

If you’re searching online for “find a mortgage broker near me,” you’re not alone and you’re in the right place. Whether you’re buying your first home, refinancing, or investing in property, a mortgage broker can make all the difference. In this guide, we’ll walk you through how to find a trusted mortgage broker in the UK, what to look out for, and how we at Mortgage Brokers Near Me help thousands of people secure the right mortgage deal every year.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR