Buying a home in the UK isn’t easy, especially with deposits rising and property prices staying high. Shared ownership mortgages were created to help people who can’t buy a whole property straight away. But how do they actually work, and what should you watch out for before diving in? Let’s break it down step by step.

Aug 18, 2025

A shared ownership mortgage is designed for people buying a share of a home rather than the full 100%. For example, you might buy 25%, 50% or 75% of a property, and a housing association owns the rest. You’ll pay your mortgage on the share you own and rent on the share you don’t.

This option can make homeownership more affordable because the deposit and mortgage are based only on your share. That means instead of saving £25,000 for a full £250,000 home, you might only need £6,250 for a 25% share.

Here’s a simple example. Let’s say you buy 50% of a house worth £200,000.

Every month, you’ll have two payments: one to your lender for the mortgage and one to the housing association for rent. Over time, if your finances improve, you can “staircase” which means buying more shares of the property. Eventually, you could own 100%.

“Shared ownership mortgages can be a great way to step onto the property ladder with a smaller deposit and manageable monthly costs.” – Will Sharman

The main appeal is affordability. Instead of waiting years to save a large deposit, you can get onto the property ladder sooner. It also opens doors to people who might otherwise be priced out of owning altogether.

But there are other reasons too. Some people see it as a flexible option. If you expect your income to rise in the future, staircasing allows you to grow your share over time.

As Will from Mortgage Brokers Near Me puts it:

“Shared ownership is right for some people. It’s about looking at your quality of life. What’s better owning 100% of a two-bed flat or 50% of a four-bed house?”

Shared ownership mortgages aren’t perfect, and it’s important to understand the downsides. For one, you’ll usually pay service charges and maintenance fees, especially in flats. These can add up quickly and make the monthly cost higher than you first expect.

Another factor is selling. If you only own part of the property, selling can take longer because the housing association often has the right to find a buyer first. Extending the lease can also be costly, which is something buyers sometimes overlook.

The process isn’t too different from a standard mortgage. You’ll still need to meet lender criteria, prove your income, and show you can afford the repayments. However, not every lender offers shared ownership mortgages, so it helps to use a broker who knows which ones to approach.

Some lenders also have rules around staircasing, lease lengths, or minimum incomes. That’s why getting advice before applying is key. At MBNM, we specialise in guiding clients through these details so nothing comes as a surprise.

Generally, shared ownership schemes are aimed at first-time buyers, people who used to own but can’t afford to buy now, or those with lower household incomes (usually under £80,000, or £90,000 in London). You’ll also need to show you don’t own another home at the time of purchase.

Shared ownership isn’t the only path to homeownership. Some people prefer to rent until they can afford a full purchase, while others look at schemes like Help to Buy or Lifetime ISAs. The best choice depends on your finances, your lifestyle, and your long-term plans.

What matters is weighing up what gives you the most stability and quality of life right now. Speaking with a mortgage advisor can help you compare the numbers clearly and see which route suits you best.

What is a shared ownership mortgage?

A shared ownership mortgage is a type of home loan where you only buy a portion of a property, usually between 25% and 75%, and pay rent on the rest. This makes it easier to get on the property ladder with a smaller deposit and lower monthly repayments compared to buying outright.

How do shared ownership mortgages work?

You take out a mortgage on the share you own and pay rent to a housing association for the share you don’t own. Over time, you can increase your ownership by buying more shares through a process called staircasing, which could eventually allow you to own 100% of the property.

How do I get a mortgage for shared ownership?

The process starts with applying for a shared ownership scheme and then finding a lender who offers these types of mortgages. Not all lenders provide shared ownership options, so working with a specialist mortgage broker can save time and help you find the best deals.

Can I increase my share later on?

Yes. Most schemes allow you to buy additional shares, known as staircasing. Each time you staircase, your rent reduces, and if you eventually own 100% of the home, you’ll stop paying rent altogether.

Are there extra costs with shared ownership mortgages?

Yes. Alongside your mortgage and rent, you may need to pay service charges, maintenance fees, and lease extension costs if applicable. These can affect the overall affordability, so it’s important to budget for them before committing.

Do all lenders offer shared ownership mortgages?

No. Only certain lenders provide mortgages for shared ownership properties, and their criteria can vary. Using a broker experienced in shared ownership can help you compare lenders, rates, and terms more easily.

“It’s not about owning a home the traditional way, but about finding a balance between affordability today and opportunities for full ownership in the future.” – Will Sharman

Shared ownership mortgages can be a good stepping stone if buying a full home feels out of reach. They make deposits smaller, monthly costs more manageable, and open the door to people who might otherwise be stuck renting. But they also come with added responsibilities like rent, service charges, and lease issues.

Before making a decision, it’s worth talking to experts who can explain the costs, lenders, and long-term implications. At Mortgage Brokers Near Me, we’ll walk you through the process, answer your questions, and help you see whether shared ownership is the right fit for you.

If you have multiple income streams, recent changes to your accounts, or you have been told your income is “too complex”, you can still get a mortgage. The key is how your income is evidenced, explained, and presented to the right lender. In this guide, we break down how lenders assess complex income, what documents you will need, when cases get declined, and how we helped a self-employed buyer secure a full mortgage offer in time to keep their property chain together.

Read Article

Yes, getting a mortgage on a zero hour contract is possible. It just takes the right guidance and lender. This blog explains what you need to qualify, how lenders view flexible income, what deposit you’ll need, and how Mortgage Broker Near Me can help you secure the best deal, even if you're self-employed, have bad credit, or work in a non-traditional role.

Read Article

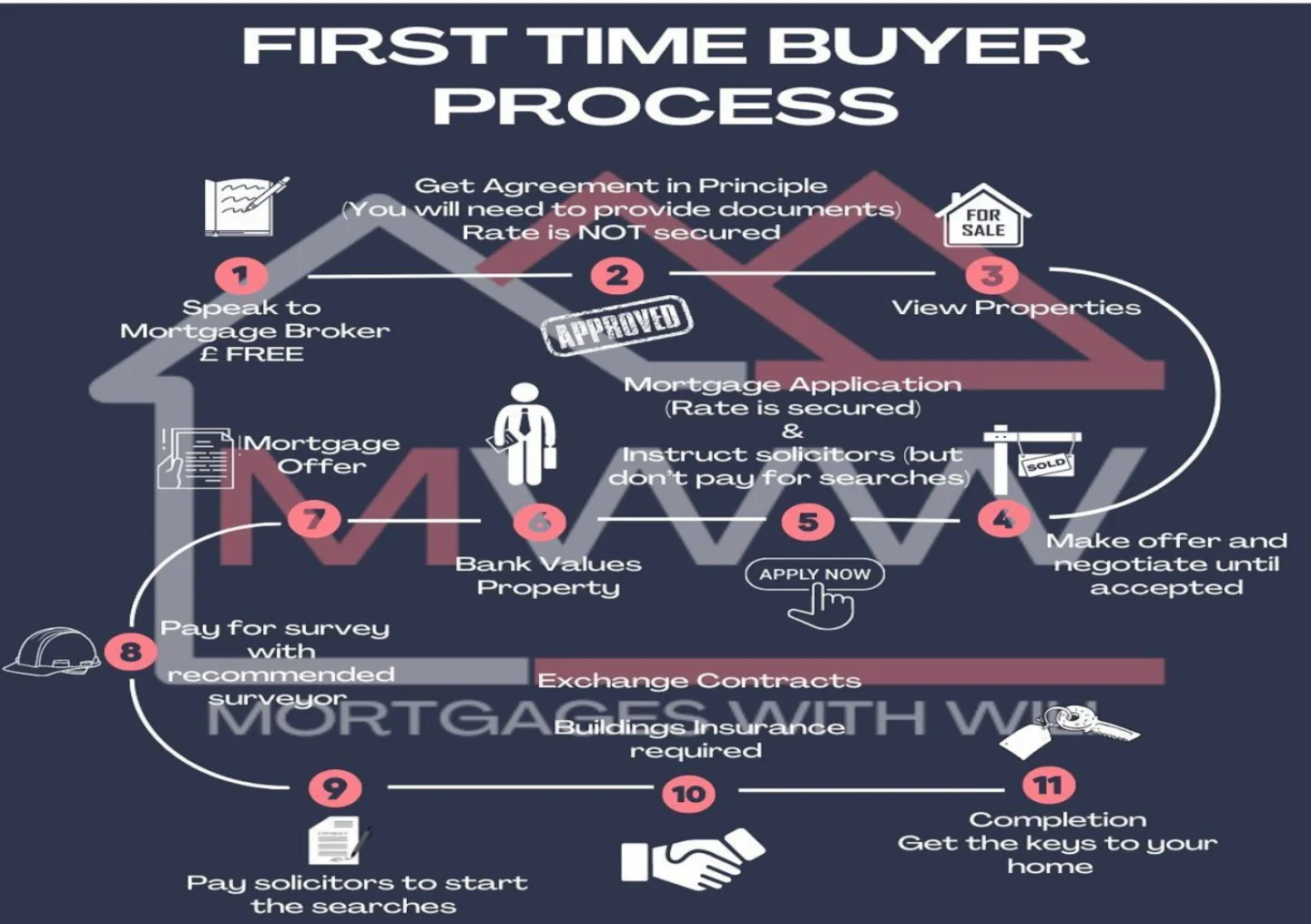

A clear, step-by-step guide to the first-time buyer process, written by Will Sharman of Mortgage Brokers Near Me. Learn what happens at each stage and when to get expert help.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR