A clear, step-by-step guide to the first-time buyer process, written by Will Sharman of Mortgage Brokers Near Me. Learn what happens at each stage and when to get expert help.

Aug 11, 2025

Buying your first home is exciting, but it can also feel overwhelming if you’ve never done it before. At Mortgage Brokers Near Me, we’ve helped countless first-time buyers navigate the process smoothly. This guide breaks it all down into simple steps so you know exactly what to expect — and when to get expert help.

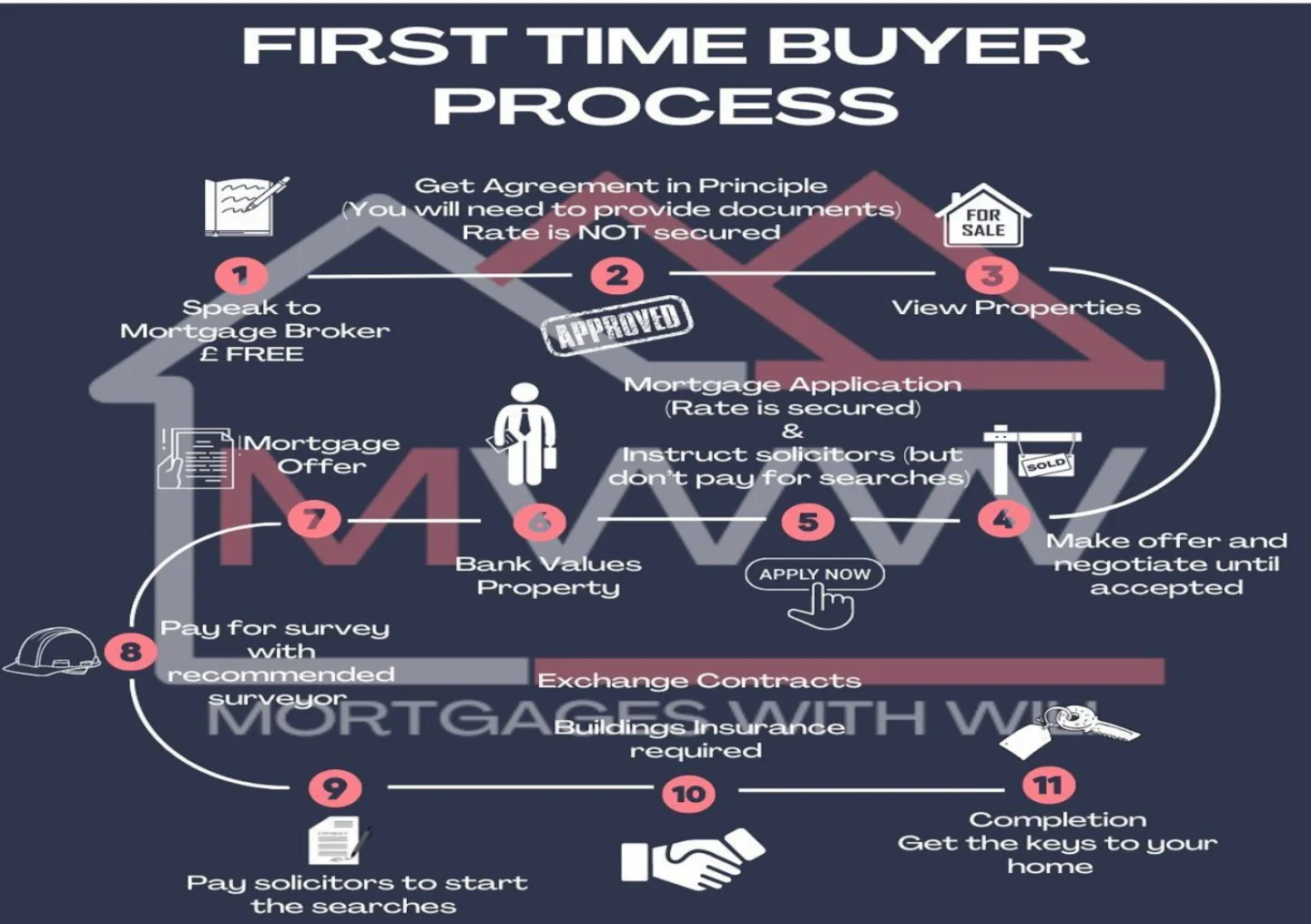

Before you start viewing properties, it’s essential to know what you can realistically afford. Speaking to a mortgage broker (like us) is free for standard residential cases and gives you a clear idea of your borrowing power. We’ll check your finances, run through your options, and save you time by comparing deals from across the market.

An Agreement in Principle (AIP) is a statement from a lender showing how much they’re likely to lend you based on your circumstances. You’ll need to provide some documents, but remember this isn’t a guaranteed mortgage offer and the rate isn’t secured at this stage. It’s mainly to show sellers you’re a serious buyer.

Buying your first home doesn’t have to feel overwhelming with the right guidance, each step becomes clear and manageable." – Will Sharman

Now the fun begins. Start viewing properties within your budget. Take notes, ask questions, and try not to get carried away it’s easy to overlook issues when you’ve fallen in love with a place. We often advise clients on what to watch out for when viewing, especially if it might affect your mortgage.

When you’ve found ‘the one,’ make your offer. Be prepared for some back and forth before it’s accepted. Remember, the estate agent works for the seller, so don’t feel pressured into rushing.

Free First-Time Buyer Guide: Download our free step-by-step guide to buying your first home, packed with tips and insider advice from experienced mortgage brokers. [Get Your Free Guide Here].

Once your offer is accepted, it’s time to submit your full mortgage application. This is when your interest rate is secured. You’ll also need to instruct a solicitor or conveyancer to handle the legal side but hold off paying for searches until your mortgage valuation is complete.

The lender will arrange a valuation to make sure the property is worth the agreed price. This is for the bank’s benefit, not yours, so it’s still worth getting your own survey later.

If everything checks out, you’ll receive a formal mortgage offer. This is your green light to move forward.

We always recommend getting a survey done so you know about any structural issues before committing. A surveyor will give you a detailed report on the property’s condition.

Once the survey results are in and you’re happy to proceed, your solicitor can start the searches checking things like planning permissions, flood risk, and local authority details.

This is when the deal becomes legally binding. You’ll also need to have buildings insurance in place from this point, as you’re now responsible for the property.

On completion day, the funds are transferred, and you finally get the keys to your new home. Time to move in and celebrate.

With years of experience helping first-time buyers, we know how to guide you through every stage of the process, avoiding delays and costly mistakes. From finding the right mortgage to liaising with solicitors and estate agents, we’re with you from start to finish.

Do I need an AIP before viewing houses?

It’s not a legal requirement, but it helps estate agents take you seriously.

How long does the whole process take?

On average, 8–12 weeks from offer to completion, but it can vary.

Can I use my own solicitor?

Yes and in many cases, it’s better to choose your own rather than one recommended by the estate agent.

What if the bank’s valuation is lower than my offer?

You may need to renegotiate the price or increase your deposit.

The earlier you speak to a mortgage broker, the smoother your home-buying journey will be." – Will Sharman

If you’re thinking about buying your first home, our team at Mortgage Brokers Near Me can help you every step of the way. We’ll find you the right mortgage, explain the process in plain English, and make sure you avoid common pitfalls.

Want to be fully prepared before you start? Grab our Free First-Time Buyer Guide and learn exactly what to expect at every stage of the process.

Get in touch today for free first-time buyer advice.

High value mortgages require more than a strong income. Lenders manually assess affordability, income sources, assets, and risk, especially for loans above £1 million. Working with the right broker early can make the difference between smooth approval and weeks of delays, reduced offers, or outright decline.

Read Article

If you’re a council tenant wondering whether you need a deposit to buy your home, the answer is often no. With the Right to Buy scheme, many lenders allow the council discount to be used as your deposit, meaning you can purchase your property without putting down cash savings. While affordability, credit history, and property type still matter, the right advice can make the difference between thinking homeownership is out of reach and actually making it happen.

Read Article

Buying a home in the UK isn’t easy, especially with deposits rising and property prices staying high. Shared ownership mortgages were created to help people who can’t buy a whole property straight away. But how do they actually work, and what should you watch out for before diving in? Let’s break it down step by step.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR