Is It Worth Going Through a Mortgage Broker? A Complete Guide for Homebuyers in Reading

Mar 18, 2025

Buying a home or refinancing a mortgage is one of the biggest financial decisions you’ll make. If you're wondering, “Is it worth going through a mortgage broker?”, you're not alone. Many homebuyers debate whether they should go directly to a bank or use a broker to find the best mortgage deal.

At Mortgage Brokers Near Me, we specialize in helping clients across Reading, Bracknell, and Wokingham secure the best mortgage rates while providing expert, impartial advice. This guide will answer:

Let’s break it down.

“A good mortgage broker doesn’t just find you a deal — they save you hours of paperwork, weeks of waiting, and thousands over the term.”

One of the most common concerns about using a mortgage broker is cost. Mortgage broker fees vary based on factors such as experience, the complexity of the case, and the lender's commission structure.

On average, mortgage brokers charge:

Fixed Fee: £300 – £600 for their services.

Percentage-Based Fee: Some charge 0.3% – 1% of the mortgage amount.

Commission-Based: Some brokers receive payment from the lender, meaning their service is free to you.

At Mortgage Brokers Near Me, we offer free mortgage advice with no hidden fees, helping you save money while securing the best deal.

Honesty is key when working with a mortgage broker. However, some statements can harm your mortgage application:

🚫 “I have no debt” – If you have credit cards or loans, be upfront about them. Lenders will see your credit report.

🚫 “I’m planning to change jobs soon” – Lenders prefer stable employment, so switching jobs mid-application can be a red flag.

🚫 “I can afford a higher monthly payment” – Your affordability is based on your income and expenses, not just what you think you can pay.

🚫 “I’m making a big purchase soon” – Avoid large expenses before mortgage approval, as it can impact your credit score and affordability.

Being transparent with your mortgage broker ensures they can find the best lender for your situation.

The best time to speak to a mortgage broker is before you start house hunting. Here’s why:

📍 Before getting a Mortgage-in-Principle – Know how much you can borrow before making an offer.

📍 If you’re self-employed or have a complex income – Get expert advice to avoid rejection.

📍 If you’re remortgaging – Compare deals to save money on your next mortgage term.

📍 If you have bad credit – A broker can help find lenders who accept lower credit scores.

By speaking to a mortgage broker early, you increase your chances of finding the best mortgage deal with minimal stress.

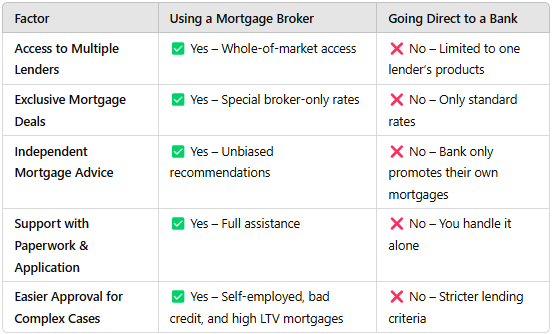

When comparing a mortgage broker to a bank, here’s what you need to consider:

While a bank may work for straightforward applications, a mortgage broker provides access to better rates, increased approval chances, and expert support—making it the smarter choice for most homebuyers.

If you're looking for easy mortgage approval, some banks are more flexible than others. Here are some of the best lenders based on different needs:

For First-Time Buyers: Halifax, Nationwide – They offer low-deposit options and government-backed schemes.

For Self-Employed Applicants: HSBC, Santander – More flexible income assessment for freelancers and contractors.

For Bad Credit: Aldermore, Kensington Mortgages – Specialize in adverse credit and non-traditional income.

For Buy-to-Let: Barclays, The Mortgage Works – Great for rental property investors.

A mortgage broker in Reading can assess your situation and find the lender that best matches your financial profile.

“Comparison sites show you options. Mortgage brokers show you what’s right for you — based on your goals, not just the rates.”

✅ If you want access to the best mortgage rates, a mortgage broker is the way to go.

✅ If you’re self-employed, have bad credit, or need help with complex applications, a broker can match you with the right lender.

✅ If you’re looking to save time and money, a mortgage broker simplifies the entire process.

At Mortgage Brokers Near Me, we compare thousands of mortgage products, ensuring you get the best deal available—completely free.

📞 Ready to find the right mortgage? Speak to an expert today!

Nationwide has changed its criteria for interest-only mortgages, and it has opened the door for more first-time buyers and homeowners to use this type of borrowing. This guide explains what the changes mean, who it helps, what to watch out for, and how to decide if it fits your plans.

Read Article

Remortgaging is basically replacing your current mortgage with a new deal, either with your existing lender or a new one. This guide explains when it’s worth doing, what you need to prepare, the steps from research to completion, the fees to watch for, and how to avoid common mistakes that cost people money.

Read Article

Yes, you can have more than one life insurance policy, and in some cases it makes a lot of sense. But it is not always the right move. This guide breaks down when having multiple policies works, when it does not, and how to decide what is right for your situation.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR