The Right to Buy discount can sometimes be used instead of a cash deposit, but it isn’t automatic. Lenders treat the discount as equity, not savings, and will still assess affordability, credit history, property type, and risk. Most Right to Buy declines happen because the case is placed with the wrong lender or key details are misunderstood, not because the scheme itself doesn’t work.

Jan 12, 2026

If you’re buying your council home under the Right to Buy scheme, you’ll hear this phrase a lot:

“Your discount can be used as your deposit.”

Sometimes that’s true.

Sometimes it absolutely isn’t.

This is where most confusion starts. Tenants get told different things by councils, banks, comparison sites, and even brokers. One lender says yes, another says no, and no one explains why.

This guide breaks down how the Right to Buy discount works as a deposit in practice, when lenders accept it, and the most common reasons applications get declined, even when the numbers look good.

Yes, in many cases the Right to Buy discount can be used instead of a cash deposit.

But lenders don’t see it as a “deposit” in the normal sense.

They see it as equity.

Here’s the difference:

Example:

If a lender is happy with the case, they may lend the full £200,000 with no cash deposit, because the equity already exists on day one.

That’s the theory.

Now let’s talk about reality.

This is the part most blogs skip.

Lenders don’t just look at the maths. They assess risk, and Right to Buy cases have several risk points that can trigger a decline.

Here are the most common ones we see.

Some lenders cap how much discount they’re willing to accept as equity.

If the discount is very large compared to the purchase price, the lender may worry about:

This is lender-specific. One bank may be fine, another may decline instantly.

Certain council properties are harder to mortgage, even with a discount.

Common problem types include:

The discount doesn’t override these issues. The property still has to be mortgageable.

Right to Buy lenders are often less forgiving than people expect.

Even with strong equity, lenders can decline if there are:

Equity helps, but it doesn’t cancel out affordability or credit risk.

This catches a lot of people out.

Even with no deposit, you still need to afford the mortgage under the lender’s stress rate.

Rising rates mean some Right to Buy cases fail affordability, especially where:

The discount does not improve affordability calculations.

Most lenders want to see:

Any gaps, disputes, or recent changes can delay or derail an application.

“No deposit” does not mean “no money at all”.

You’ll still need funds for:

Some lenders will also want to see evidence of savings, even if they’re not being used as a deposit.

This is where most buyers lose confidence.

One bank says yes. Another says no. A third won’t even look at it.

That’s because Right to Buy cases are not assessed consistently across the market.

Some lenders:

Others:

This is why lender choice matters far more than headline claims about “no deposit mortgages”.

A client came to us living in a council property, never expecting to own it.

They’d been told by others it wasn’t possible.

We structured the case correctly, selected a lender that accepted the discount as equity, and raised the full £200,000 purchase price with no cash deposit.

The difference wasn’t the scheme.

It was how the case was presented and where it was placed.

Right to Buy discount cases tend to succeed when:

When those line up, the discount can work exactly as people hope.

At Mortgage Brokers Near Me, we don’t treat Right to Buy as a generic product.

We look at:

That’s how we prevent avoidable declines and keep expectations grounded in reality.

The Right to Buy discount can act as your deposit.

But it isn’t automatic, guaranteed, or universal.

When lenders say no, it’s rarely because the scheme doesn’t work. It’s because something in the case doesn’t fit that lender’s rules.

Understanding that difference is what turns confusion into a mortgage offer.

Can I get a joint mortgage with an IVA? Yes – but it depends on the IVA’s status, your deposit size, and your partner’s credit profile. This guide from Will Sharman at Mortgage Brokers Near Me explains how joint mortgages work with an IVA, which lenders might accept you, and what to expect during the process. Includes FAQs, real-life examples, and expert tips to boost your approval chances.

Read Article

If you’re searching online for “find a mortgage broker near me,” you’re not alone and you’re in the right place. Whether you’re buying your first home, refinancing, or investing in property, a mortgage broker can make all the difference. In this guide, we’ll walk you through how to find a trusted mortgage broker in the UK, what to look out for, and how we at Mortgage Brokers Near Me help thousands of people secure the right mortgage deal every year.

Read Article

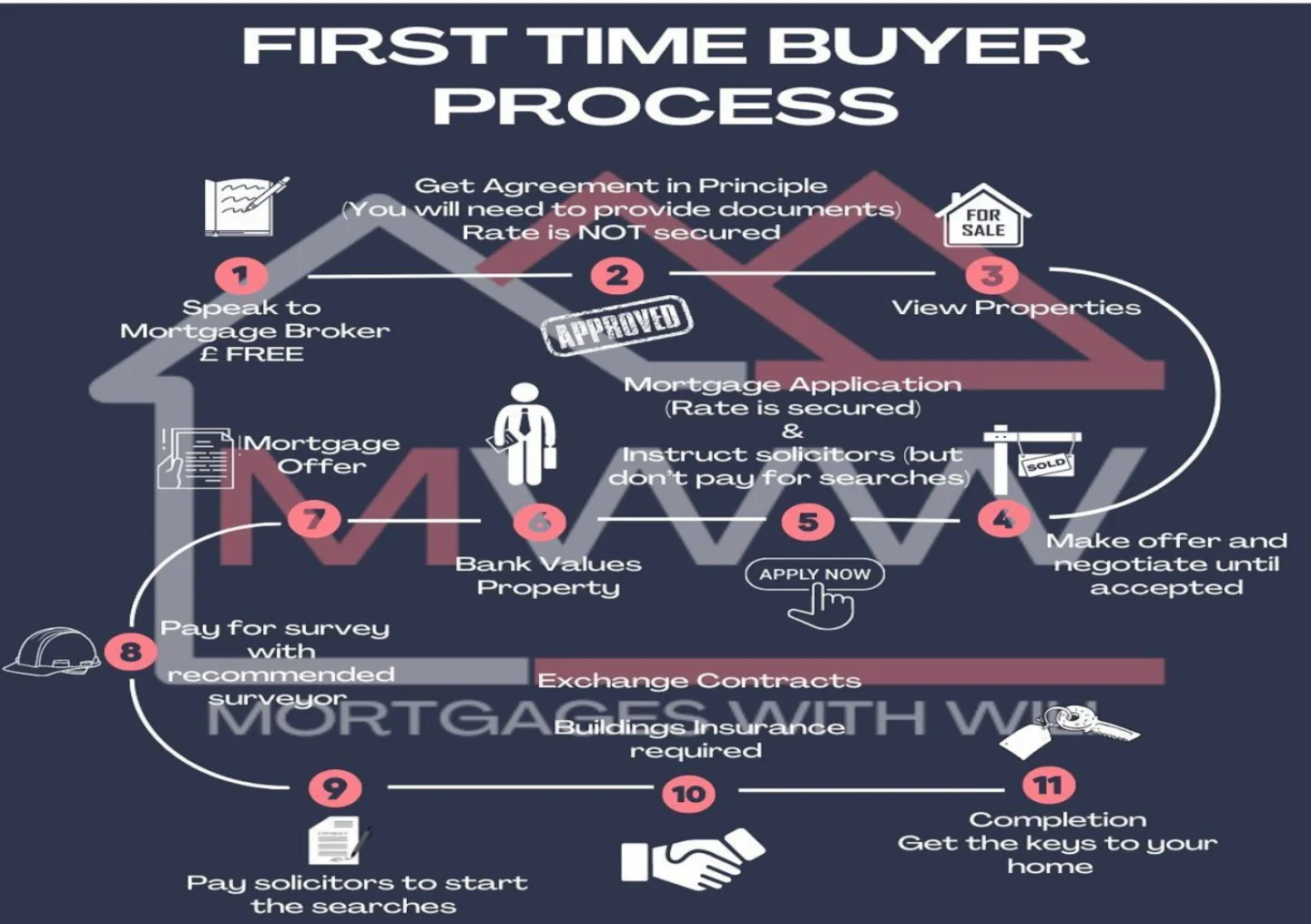

A clear, step-by-step guide to the first-time buyer process, written by Will Sharman of Mortgage Brokers Near Me. Learn what happens at each stage and when to get expert help.

Read ArticleIf you’re buying, moving, or remortgaging, speak with a MBNM adviser and get clear guidance on what’s realistically available to you, before you commit to anything.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Mortgage Brokers Near Me LTD is an Appointed Representative of The Right Mortgage LTD which is authorised and regulated by the Financial Conduct Authority.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK. The Financial Conduct Authority does not regulate Will Writing and some forms of Trusts and Buy to Lets. A fee may be charged for mortgage advice. The exact amount will depend on your circumstances.

Mortgage Brokers Near Me LTD are registered in England and Wales with company number 15189091.

C/O The Financial Management Centre, Meads Business Centre, 19 Kingsmead, Farnborough, England, GU14 7SR